LATIN AMERICA

TTR Deal Tracker is a monthly email update identifying M&A trends in Latin America and compiling YTD rankings of leading financial and legal advisors

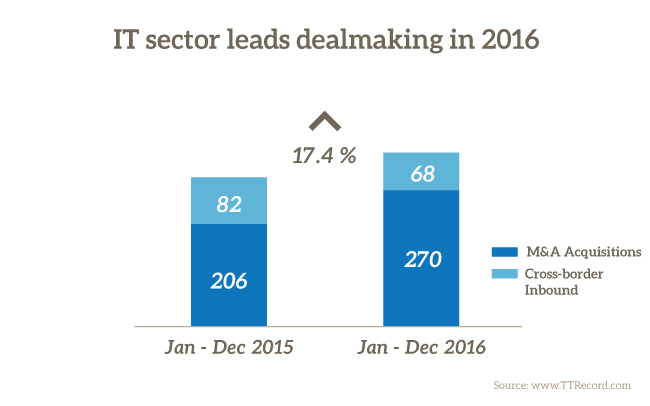

BRAZIL: IT sector leads dealmaking in 2016

Transactions in Brazil’s IT sector led dealmaking in 2016 with volume up 17% over the previous year, according to TTR data (www.TTRecord.com).

The number of cross-border deals in the space led by international buyers fell slightly, meanwhile, from 82 in 2015 to 68 in 2016. As in 2015, North American bidders demonstrated the strongest appetite for Brazilian firms from among the pool of foreign investors targeting the space.

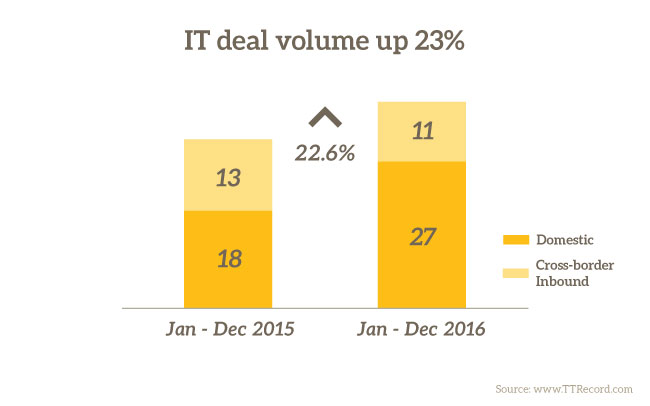

MEXICO: IT deal volume up 23%

Dealmaking in Mexico’s IT space was up 23% in 2016 over the previous year, according to TTR data (www.TTRecord.com).

The number of transactions led by foreign buyers fell slightly from 13 in 2015 to 11 in 2016, meanwhile. The largest deal in the space in 2016 was the USD 55m capital injection in e-commerce company Linio.

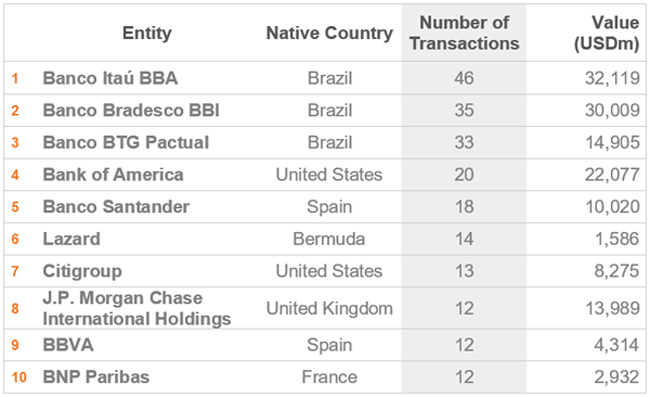

Latin America Ranking – 2016*

Financial Advisory by number

Banco Itaú BBA leads TTR’s Latin America financial advisory ranking for 2016 with 46 deal mandates for the year on transactions worth a combined USD 32.1bn. Itaú’s 2016 performance represents a 13% dip in deal volume and a 55% spike in aggregate value compared to its 53 mandates on deals worth a combined USD 20.7bn in 2015, when it also led the chart. Banco Bradesco BBI climbed from third in 2015 to take second place in 2016 region-wide, its volume up 67% from 21 to 35 deals, the aggregate value of those transactions up 145% from USD 12.3bn to USD 30bn. Banco BTG Pactual was bumped from second in 2015 to third in 2016, meanwhile, its deal volume down 18% from 40 to 33, its aggregate value down 4% from USD 15.5bn to USD 14.9bn. BAML grew its deal volume 186% to place fourth while the aggregate value of its transactions climbed 1,494% to USD 22bn after not placing among the top 10 regionally for full year 2015. Banco Santander fell one place in the chart to take fifth despite increasing volume 50% from 12 to 18 and upping aggregate value 25% from USD 8bn to USD 10bn between the two twelve-month periods. Lazard, in sixth with 14 deals worth a combined 1.6bn, did not place among the top 10 regionally in 2015, nor did Citigroup, in seventh with 13 mandates on deals together worth USD 8.3bn, nor JPMorgan, in eighth with 12 worth USD 14bn combined. BBVA fell three positions to take ninth, despite adding one deal to its count and the aggregate value of it deals increasing 205% from USD 1.4bn to USD 4.3bn. BNP Paribas, in tenth, also with 12 mandates for the year in the region, was not among the top 10 financial advisors in Latin America in 2015.

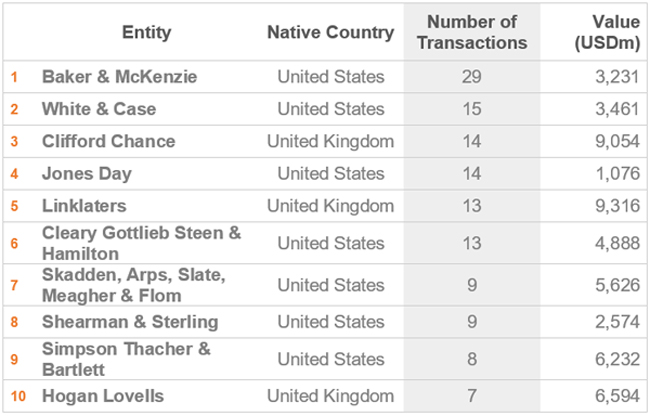

Latin America Ranking* – 2016

Legal Advisory by number

Baker & McKenzie leads TTR’s Latin America legal advisory ranking for 2016 with 29 mandates on deals together worth USD 3.2bn, representing a 12% drop in volume and a 50% increase in aggregate value compared to its performance the previous year, when it also led the chart. White & Case follows in second, its deal count up by two to 15, the aggregate value of its transactions up 158% from USD 1.3bn to USD 3.5bn relative to its 2015 performance when it placed third. Clifford Chance also climbed one position in the chart to take third, its 14 deals worth a combined USD 9bn, representing a 56% increase in volume and a 6% increase in aggregate value compared to its nine together worth USD 8.5bn in 2015. Jones Day fell two positions from second to take fourth, its deal volume down by 10 to 14, its aggregate value down 61% from USD 2.8bn to USD 1bn. Linklaters is up three positions in the ranking from eighth to fifth, its deal count nearly doubling from seven to 13, the combined value of its transactions up nearly 4,000% from USD 233m to USD 9.3bn. Cleary Gottlieb Steen & Hamilton also advised on 13 deals in 2016, in its case worth a combined USD 4.9bn, after not placing among the top 10 legal advisors in Latin America in 2015. Skadden, Arps, Slate, Meagher & Flom, ranked seventh, advised on nine deals in 2016, the same volume as in 2015, while the aggregate value of its transactions increased 372% from USD 1.2bn to USD 5.6bn. Shearman & Sterling fell three positions to take eighth, its deal volume remaining constant, its aggregate value up 109% from USD 1.2bn to USD 2.6bn. Simpson Thacher & Bartlett is up one place in the chart in ninth after adding three deals to its count in 2015 while its aggregate deal value fell 2% from USD 6.4bn to USD 6.2bn. Hogan Lovells, in tenth with seven deals worth a combined 6.6bn, was not among the top 10 in 2015.

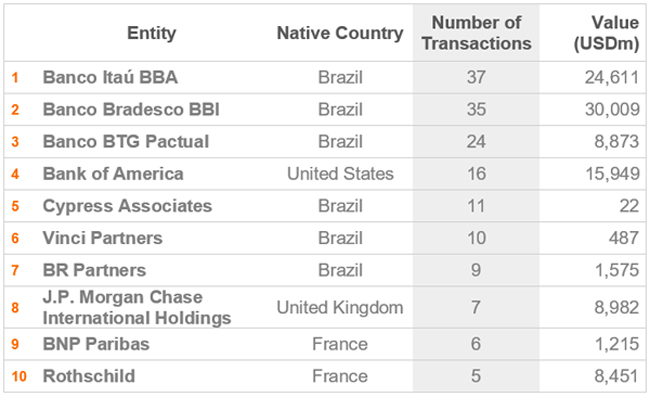

Brazil Ranking* – 2016

Financial Advisory

Banco Itaú BBA leads TTR’s Brazil financial advisory ranking for 2016 with 37 mandates on deals worth a combined USD 24.6bn. Brazil’s top investment bank also led the chart in 2015 when it’d advised on 46 deals worth a combined 20bn, representing a 20% decline in volume and a 23% increase in aggregate value. Banco Bradesco BBI is up one place in the chart to take second, its volume increasing 75% from 20 to 35, its aggregate value up 145% from USD 12.3bn to USD 30bn. Banco BTG Pactual fell one place to take third, its volume down 17% from 29 to 24, its aggregate value down 37% from USD 14bn to USD 8.9bn. BAML ranks fourth with 16 deals worth a combined USD 15.9bn after not placing among the top 10 investment banks in Brazil for full year 2015. Cypress Associates, in fifth with 11 deals together worth USD 22m, was also absent from the top 10 in 2015. Vinci Partners ranks sixth, as it did in 2015, its deal count increasing by one, its aggregate value up 164% from USD 184m to USD 487m. BR Partners fell two positions in the chart to take seventh, its volume on par at nine, its aggregate value up 353% from USD 347m to USD 1.6bn. JPMorgan, in eighth with seven deals for the year worth a combined USD 9bn, was not among the top ten in 2015, nor was BNP Paribas in ninth with six deals together worth USD 712m. Rothschild fell one place in the chart to take tenth, its deal count falling by one, its aggregate value up 3% from USD 8.2bn to USD 8.5bn.

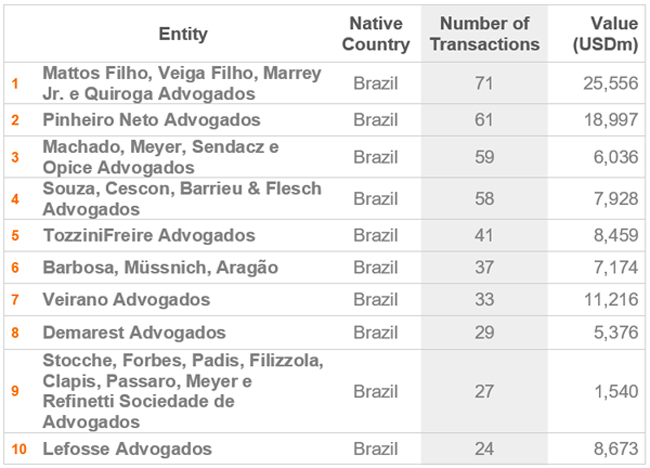

Brazil Ranking* – 2016

Legal Advisory

Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados leads TTR’s Brazil legal advisory ranking for full year 2016 with 71 transactions worth a combined USD 25.6bn, representing a 20% increase in volume and a 99% jump in aggregate value from the 59 deals together worth USD 12.9bn in 2015 when it ranked second. Pinheiro Neto Advogados fell from its leadership position in 2015 to rank second, its volume down 9% from 67 to 61, its aggregate value down 7% from USD 20.4bn to USD 19bn. Machado, Meyer, Sendacz e Opice Advogados ranks third with 59 deals worth a combined USD 6bn, up 16% by volume, down 73% by aggregate value compared to its performance in 2015, when it also ranked third. Souza, Cescon, Barrieu & Flesch Advogados ranks fourth, as it did for full year 2015, its deal count up from 51 to 58, the combined value of its deals up 18% from USD 6.7bn to USD 7.9bn. TozziniFreire Advogados climbed three positions in the chart to take fifth, its volume up by 10 to 41, its aggregate value up by 867% from USD 875m to USD 8.5bn. Barbosa, Müssnich, Aragão is down one position in the chart in sixth, its deal count down from 45 to 37, its aggregate value down 39% from USD 11.8bn to USD 7.2bn. Veirano Advogados, in seventh, also fell one place in the chart, its volume down 23% from 43 to 33, its aggregate value up 647% from USD 1.5bn to USD 11.2bn. Demarest Advogados too is down one place in the ranking, its volume having declined 24% from 38 to 29 while the aggregate value of its deals rose 178% from USD 1.9bn to USD 5.4bn. Stocche, Forbes, Padis, Filizzola, Clapis, Passaro, Meyer e Refinetti Sociedade de Advogados ranks ninth with 27 mandates in 2016 worth a combined 1.5bn, after not placing among the top 10 for full year 2015. Lefosse Advogados, in tenth with 24 deals together worth USD 8.7bn, was also absent from the top 10 in 2015.

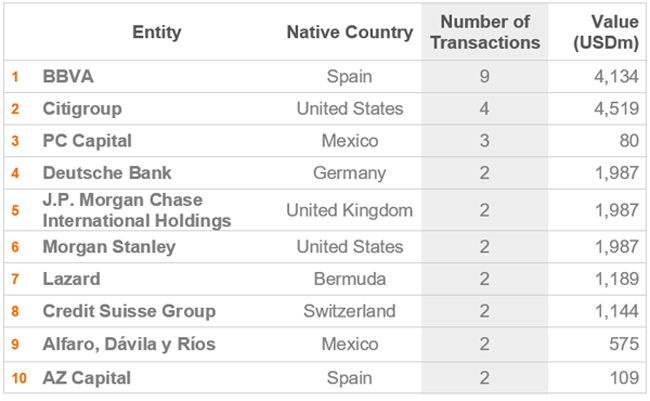

Mexico Ranking* – 2016

Financial Advisory

BBVA leads TTR’s Mexico financial advisory ranking for full year 2016 with nine deals worth a combined USD 4.1bn, up from seven together worth USD 960m in 2015 when it also led the chart. Citigroup ranks second with four transactions worth a combined USD 4.5bn, leading the chart by aggregate value after not ranking among the top 10 for full year 2015. PC Capital ranks third, as it did the previous year, its deal count down by one to three. Deutsche Bank, in fourth with two deals in 2016, is tied by volume with JPMorgan, Morgan Stanley, Lazard, Credit Suisse Group, Alfaro, Dávila y Ríos and AZ Capital. Of the lot, only Lazard and Alfaro, Dávila y Ríos ranked among the top 10 in 2015, also with two transactions each. Lazard ranked sixth for full year 2015, its two deals amounting to USD 1bn combined, compared to USD 1.2bn in 2016, while Alfaro, Dávila y Ríos ranked fifth, its two transactions together worth USD 2.2bn, compared to USD 575m a year later.

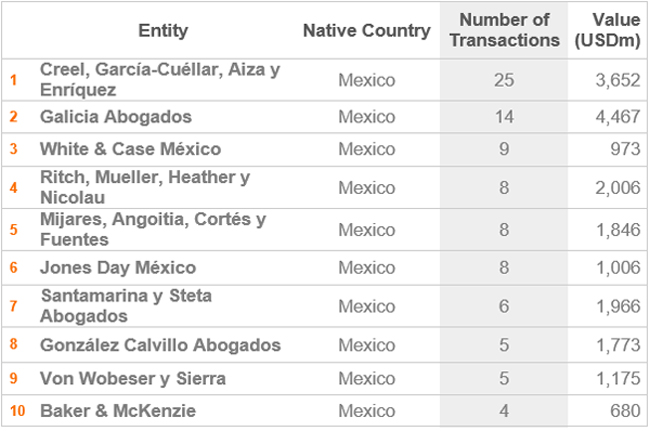

Mexico Ranking* – 2016

Legal Advisory

Creel, García-Cuéllar, Aiza y Enríquez leads TTR’s Mexico legal advisory ranking for full year 2016 with 25 mandates on deals worth a combined USD 3.7bn, representing a 7% decline in volume and a 74% drop in aggregate value compared to its 27 transactions together worth USD 14bn in 2015, when it also topped the chart. Galicia Abogados is up one position in second with 14 deals worth a combined USD 4.5bn, on par by volume and up 57% by aggregate value compared to its performance for full year 2015, when it ranked third. White & Case México climbed one position in the chart to third, despite a slight decline in volume from 11 to nine transactions and a 26% drop in aggregate value from USD 1.3bn to USD 973m. Ritch, Mueller, Heather y Nicolau, in fourth with eight deals worth a combined USD 2bn, was not among the top 10 for full year 2015. Mijares, Angoitia, Cortés y Fuentes ranks fifth, also with eight advisory mandates in 2016, down from 15 in 2015 when it ranked second, while the firm’s aggregate deal value dipped 23% from USD 2.4bn to USD 1.8bn. Jones Day México is down one position in the chart in sixth, its deal count down by two to eight, its aggregate value down 55% from USD 2.2bn to USD 1bn. Santamarina y Steta Abogados, absent from the top 10 ranking for 2015, advised on six transactions in 2016 to place seventh, its deals together worth USD 2bn. González Calvillo Abogados, in eighth, is tied by volume with Von Wobeser y Sierra, the former’s five worth USD 1.8bn combined, the latter’s together worth USD 1.2bn. Neither firm was among the top 10 for 2015. Baker & McKenzie México fell four positions to bring up the rear with four transactions in 2016, half the volume of the previous year, while its aggregate value increased 86% from USD 366m to USD 680m.

* TTR Rankings are generated with transactions announced or closed in 2016 year-to-date. The ranking includes sales and acquisitions of shares and of assets, creation of joint ventures, and Private Equity/Venture Capital investments. The legal advisor rankings for Brazil and Mexico take into consideration advisory services regarding domestic laws. All rankings only include deals where a company of the respective country was the target of the transaction. In the case of LATAM, it would be a Latin American country. The LATAM ranking does not specify the origin of the advisory law, so the filter only considers firms from the UK/US.

In case of a draw, the adopted criteria will be the following: if the draw is due to number of transactions, the total deal value prevails; if it is due to deal value, the number of transactions prevail. When a draw of both number of transactions and deal value occurs, the same position will be retained and the deals will be arranged alphabetically.